How to Crack a Nut will be back on 20 August 2012, hopefully with renewed energies for the last quarter of this intense year. In the meantime, happy holidays to everyone!

This is a blog about the use of emerging technologies to boost the governance of public procurement. It used to be a blog on EU law, with a focus on free movement, public procurement and competition law issues (thus the long archive of entries about those topics). I use it to publish my thoughts and to test some ideas. All comments are personal and in no way bind any of the institutions to which I am affiliated and, particularly, the University of Bristol Law School. I hope to spur discussion and look forward to your feedback and participation.

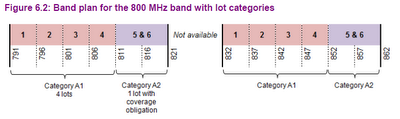

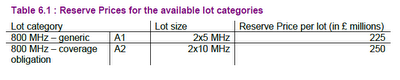

A reasonable estimate of the cost of a 98% population coverage obligation should range from £100m to £400m as the cost estimate provided by Vodafone (and supported by O2) of £540m may not reflect the cost of meeting the coverage obligation by an operator with a well maintained, efficient network: John Cresswell of Arqiva estimated that the [98%] coverage obligation will cost around £200m to £230m, with Guy Laurence of Vodafone stating that a further £140 million in operating expenditure would be required to achieve 99% coverage (emphasis added; please note that £200 million is precisely the implicit discount in the reduced reservation price for lot "5 & 6").

State control, such as that observed in the present case [where the distribution of the shares allowed the State shareholders to control the undertaking], cannot be equated, as a matter of principle, to ‘significant State interference’ within the meaning of the first indent of Article 2(7)(c) of [Council Regulation (EC) No 384/96 of 22 December 1995 on protection against dumped imports from countries not members of the European Community, as amended by Council Regulation (EC) No 461/2004 of 8 March 2004] and cannot therefore relieve the Council and the Commission of the obligation to take into account the evidence, submitted by the producer concerned, of the real factual, legal and economic context in which it operates (Xinanchem at para. 78).

the fact that a precise scale of the calculation of the tenders with regard to that award criterion [multiplication of efficiency by effectiveness] was not given cannot constitute a breach of the tendering specifications consisting in the introduction, by the contracting authority, of a new award criterion. The calculation used to arrive at a well defined score does not constitute an evaluation criterion of the proposed hypothetical IT solution, but rather a consequence of that evaluation (case T-476/07, at para 106, emphasis added).

[...] the activity of a public authority consisting in the storing, in a database, of data which undertakings are obliged to report on the basis of statutory obligations, in permitting interested persons to search for that data and/or in providing them with print-outs thereof does not constitute an economic activity, and that public authority is not, therefore, to be regarded, in the course of that activity, as an undertaking, within the meaning of Article 102 TFEU. The fact that those searches and/or that provision of print-outs are carried out in consideration for remuneration provided for by law and not determined, directly or indirectly, by the entity concerned, is not such as to alter the legal classification of that activity (Compass-Datenbank at para. 51).

In the light of the entirety of that case-law, it must be observed that a data collection activity in relation to undertakings, on the basis of a statutory obligation on those undertakings to disclose the data and powers of enforcement related thereto, falls within the exercise of public powers. As a result, such an activity is not an economic activity.

Equally, an activity consisting in the maintenance and making available to the public of the data thus collected, whether by a simple search or by means of the supply of print-outs, in accordance with the applicable national legislation, also does not constitute an economic activity, since the maintenance of a database containing such data and making that data available to the public are activities which cannot be separated from the activity of collection of the data. The collection of the data would be rendered largely useless in the absence of the maintenance of a database which stores the data for the purpose of consultation by the public (Compass-Datenbank at paras. 40 and 41, emphasis added).

[...] a public entity which creates a database and which then relies on intellectual property rights, and in particular the abovementioned sui generis right, with the aim of protecting the data stored therein, does not act, by reason of that fact alone, as an undertaking. Such an entity is not obliged to authorise free use of the data which it collects and make available to the public. [...] a public authority may legitimately consider that it is necessary, or even mandatory in the light of provisions of its national law, to prohibit the re-utilisation of data appearing in a database such as that at issue in the main proceedings, so as to respect the interest which companies and other legal entities which make the disclosures required by law have in ensuring that no re-use of the information concerning them is possible beyond that database (Compass-Datenbank at para. 47, emphasis added).

The fact that the making available of data from a database is remunerated does not have any bearing on whether a prohibition on the re-use of such data is or not economic in nature, provided that that remuneration is not itself of such a nature as to enable the activity concerned to be classified as economic [...]. To the extent that the remuneration for the making available of data is limited and regarded as inseparable from it, reliance on intellectual property rights in order to protect that data, and in particular to prevent its re-use, cannot be considered to be an economic activity. Such reliance is, accordingly, inseparable from the making available of that data (Compass-Datenbank at para. 49, emphasis added).

47 [...] article 8(5) of Regulation No 207/2009 covers three separate and alternative types of risk, namely that the use without due cause of the mark applied for will take unfair advantage of the distinctive character or the repute of the earlier mark, or that it will be detrimental to the distinctive character of the earlier mark, or that it will be detrimental to the repute of the earlier mark.48 The unfair advantage taken of the distinctive character or the repute of the earlier trade mark consists in the fact that the image of the mark with a reputation or the characteristics which it projects will be transferred to the goods covered by the mark applied for, with the result that the marketing of those goods can be made easier by that association with the earlier mark with a reputation.49 It should, however, be emphasised that in none of those cases is it necessary that there be a likelihood of confusion between the marks at issue; it is only necessary that the relevant public is able to establish a link between them, without having necessarily to confuse them [...]56 [...] The advantage arising from the use by a third party of a sign similar to a mark with a reputation is an advantage taken unfairly by that third party of the distinctive character or the repute of the mark where that party seeks by that use to ride on the coat-tails of the mark with a reputation in order to benefit from the power of attraction, the reputation and the prestige of that mark and to exploit, without paying any financial compensation, the marketing effort expended by the proprietor of the mark in order to create and maintain the mark’s image

59 With regard to the goods and services in the present case, those of the applicant do not appear to be directly and immediately linked to the intervener’s theatre productions. However, despite the differences in the nature of those goods and services, there is, none the less, a certain proximity and link between them. In that regard, it has already been acknowledged in case-law that there is a certain similarity between entertainment services and beer due to their complementarity (see Judgment of 4 November 2008 in Case T‑161/07 Group Lottuss v OHIM – Ugly (Coyote Ugly), not published in the ECR, paragraphs 31 to 37). It is common practice, in theatres, for bar and catering services to be offered either side of and in the interval of a performance. (emphasis added)60 Moreover, irrespective of the above, in view of the established reputation of the earlier trade mark, the relevant public, namely the public at large in the United Kingdom, would be able to make a link with the intervener when seeing a beer with the contested trade mark in a supermarket or in a bar.61 In the present case, the applicant would benefit from the power of attraction, the reputation and the prestige of the earlier trade mark for its own goods, such as beer and other beverages, and for its services. In the beverages market, those goods would attract the consumer’s attention thanks to the association with the intervener and its earlier trade mark, which would give the applicant a commercial advantage over its competitors’ goods. That economic advantage would consist of exploiting the effort expended by the intervener in order to establish the reputation and the image of its earlier trade mark, without paying any compensation in exchange. That equates to an unfair advantage taken by the applicant of the repute of the earlier trade mark within the meaning of Article 8(5) of Regulation No 207/2009.